The Ginnie Mae Issuer and MBS Disclosures

By Sharad Chaudhary

Ginnie Mae (GNMA) does not report seller or servicer information for its pools or loans; instead, associated with each GNMA pool/loan is the notion of an Issuer. Indeed, GNMA's conception of the Issuer role doesn't map straightforwardly to the standard functions performed by the sellers and servicers associated with GSE pools since the Issuer's responsibilities are prescribed to encompass those of the mortgage owner, the pool issuer, and the servicer.[1] At a high level, these duties are:

- Acquiring or originating eligible mortgages under the guidelines of the respective FHA, VA, RHS, and PIH programs.

- Forming eligible pools or loan packages in conformance with GNMA guidelines.

- Servicing the mortgages in the pool or loan package or, where permitted, contracting with a subservicer.[2] This includes making timely payments and covering shortfalls. While this nominally appears to be the same role as GSE servicers perform, the GNMA issuer has more responsibility and greater financial exposure to delinquent loans [Kaul2020]:

- Creating and maintaining proper P&I and escrow custodial accounts; ensuring that payments and other funds relevant to the pooled mortgages are properly handled.

- Acquiring an eligible document custodian[3] for all documents related to a pool or loan package; providing these documents to the document custodian and the pool processing agent (PPA);[4] ensuring that custodial documents are securely maintained when in the Issuer's possession. The custodial role carries magnified importance by virtue of the fact that Ginnie Mae ultimately bears issuer credit risk and requires proper documentation to legally acquire and transfer loans from a defaulted issuer to another issuer (or sometimes itself).

- Marketing or holding the securities backed by the pool or loan package.

Issuer Servicing Transfers

The most important responsibility of the Issuer is servicing loans and, subject to approval, GNMA does allow an Issuer to transfer their servicing responsibilities in two distinct ways:

- A bulk transfer of mortgage-servicing rights (MSRs); or,

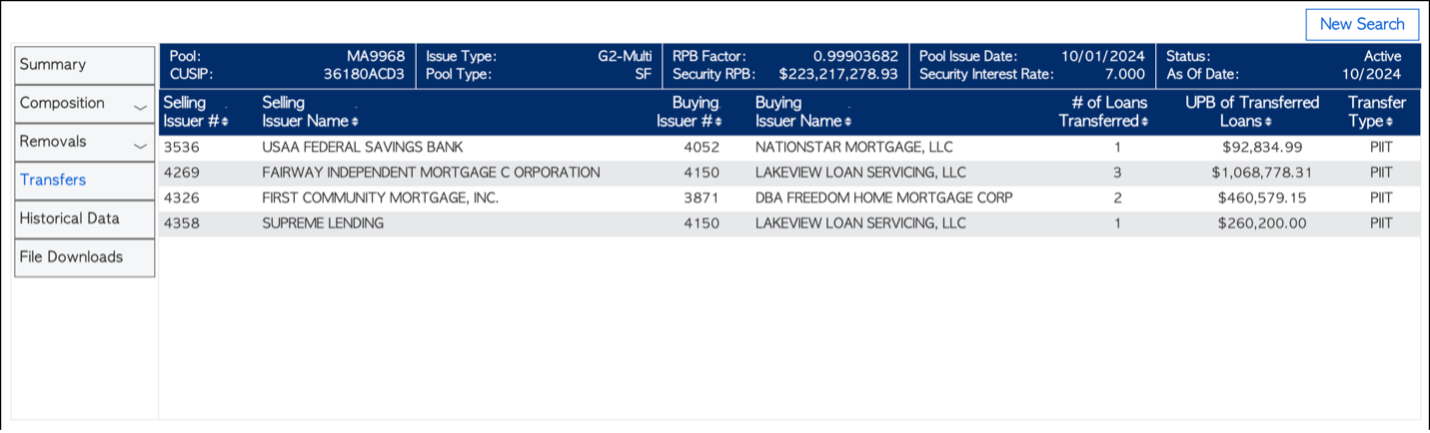

- A flow transfer of MSRs through the Pool Issuance for Immediate Transfer (PIIT) program.[5]

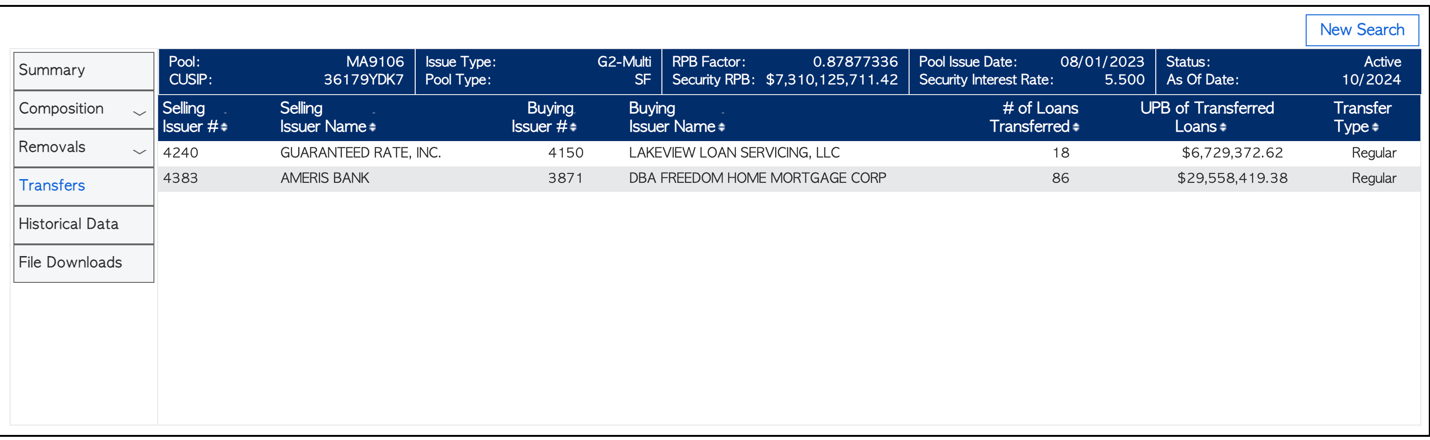

Similarly, here's an example of a bulk transfer for a GNMA II Multiple-Issuer Pool (MIP):

Issuer Data in GNMA MBS Disclosures

Given the critical role played by Issuers, GNMA releases several different disclosures that allow MBS holders to identify and track the various entities associated with different types of GNMA pools. Specifically, there are three different Issue Types associated to GNMA pools: single-issuer pools with an issue type of "X" (GNMA I pool) or "C" (GNMA II Custom), and multiple-issuer pools to which one or more participating issuers contribute a loan package that have an issue type of "M" (GNMA II MIPs). We now summarize the main pool-level disclosures of issuer data while contrasting how data is disclosed for single- versus multiple-issuer pools:

- An issuer file is released on the 4th Business Day (BD4) every month; this file has a list of issuer numbers and the corresponding issuer name,[7] and only contains data for issuers of current Ginnie Mae pools and loans (i.e., it is not a master file).

- The release of pool-level issuer data (issuer number and name, outstanding balances and loan counts) is distributed over different file types (pool/security files, supplemental files, factor files) and different business days (BD1, BD4, BD6, and BD8):

The loan-level disclosures of issuer data are:

- The issuer number of the current issuer (disclosed on BD1, BD4[10], and BD6)

- The transfer issuer number: the issuer number of the selling issuer if servicing is transferred in the current month (BD1, BD6). However, the transfer issuer number is set to NULL for BD1 records even in cases where servicing for the loan has been released through a PIIT.

Inferring the Seller/Servicer through GNMA Issuer Disclosures

As remarked above, there is no formal concept of a "seller" for GNMA pools but in order to harmonize naming conventions across Agency MBS, we define the GNMA "seller" to be the Issuer at-origination. Assuming this convention, inferring the servicer(/s) and seller(/s) of loans in Ginnie pools is not always straightforward. Clearly, one rule is that the issuer name corresponds to both the seller and the servicer of the GNMA pool/loan package as long as a transfer has not occurred. If a transfer does occur:

- The issuer name typically represents the current servicer for single-issuer pools unless it's the at-issue record in which case it's still the selling issuer and transfer detail records must be referenced to infer who the current servicer is.

- For MIPs, we initially record the servicer and seller to be the same for the at-issue record. If the issuer name changes in the next record, we know that a PIIT has occurred because there's a 30-day stay on Bulk Transfers starting from the pool or loan package issuance date.[11] In that case, we can update the at-issue servicer with the current issuer name.

- Servicer distributions for MIPs are captured in the issuer detail supplemental record but existing seller distributions are no longer easy to track after the at-issue record using pool-level data because Ginnie pool-level transfer disclosures are at the issuer- and not loan-level.[12] However, seller distributions can be tracked using loan-level data.

Notes

[1] See [CBO2022], Chapter 4 in [GNMAGuide], [Kaul2020], and [Tozer2019] for further details.

[2] When a subservicer is appointed, the Issuer is still ultimately responsible to ensure that the servicing meets GNMA standards.

[3] The document custodian reviews the loan documents submitted by the Issuer for each pool/loan package and certifies to Ginnie Mae that they accurately represent the pooled mortgages and that they capture Ginnie Mae requirements. The custodian holds the loan documents in safekeeping for the life of the pool or loan package.

[4] The Pool Processing Agent (PPA) reviews and approves on Ginnie Mae's behalf, the physical documents and/or electronic transmissions submitted by the Issuer that describe the pool/loan package. Upon approving the pool/loan package, the PPA directs that the securities be issued. The PPA also certifies that the appropriate accompanying documents for a pool/loan package have been submitted and that they are correct (see Chapter 11 of the GNMA MBS Guide).

[5] Servicing is recorded in the name of the PIIT buyer at the time of issuance.

[6] Not all pool types are eligible for PIIT; for example, HMBS pools are ineligible.

[7] Since there is no single issuer associated with a MIP, Ginnie Mae uses the issuer number of 9999 to denote the presence of multiple issuers for "M" pools.

[8] GNMA does not currently release at-issue records for Platinums.

[9] No transfer detail records are available for Platinums.

[10] Only for liquidated loans.

[11] Section D(2), Part 4, Chapter 11 of Ginnie Mae MBS Guide. One implication of the 30-day holding period after acquiring servicing is that bulk servicing transfers can only take place in the 3rd month after pool/package issuance.

[12] Concretely, if issuer A owns servicing for 10 loans at issuance and transfers/sells 5 of them to Issuer B through a PIIT then by the next reporting period it is not necessarily clear what the seller distribution is. Since the 5 loans that went to Issuer B are not individually identified in the data, in the next reporting period they can no longer be distinguished if some of the loans in Issuer B's initial contribution to the MBS prepaid in the interim. In other words, we have no way of knowing which of the surviving loans should be mapped to Issuer A or Issuer B as a seller in this situation.

References

[CBO2022] Congressional Budget Office, Ginnie Mae and the Securitization of Federally Guaranteed Mortgages, https://www.cbo.gov/publication/57755

[GNMAGuide] Ginnie Mae, MBS Guide, https://www.ginniemae.gov/issuers/program_guidelines/Pages/mbs_guide.aspx

[Kaul2020] Karan Kaul and Ted Tozer, The Need for a Federal Liquidity Facility for Government Loan Servicing (Urban Institute, July 2020), https://tinyurl.com/3c6b2exm

[Tozer2019] Ted Tozer, A Primer and Perspective on Ginnie Mae (Milken Institute, October 2019), https://tinyurl.com/54kw29fm